José Antonio Montenegro interviews Natalia Fabra for Globoeconomía (CNN en Español), a CNN production by Warner Bros. Discovery.

They discuss the urgent need to triple investments in renewables and energy storage to meet the rising electricity demand driven by electrification and the expansion of data centers.

Natalia also highlights the importance of developing common metrics to measure emissions and climate risks, enabling companies to better evaluate the profitability of adaptation investments, and helping banks to channel funds toward the most effective projects.

The conversation touches on the key challenges of the energy transition — renewables, storage, grid infrastructure, green hydrogen, and incentives for firms and households to adopt clean technologies.

In an opinion column for El País, Natalia Fabra challenges the claim that keeping nuclear plants open is essential for Spain’s energy security and affordability. She argues that a well-managed renewable rollout—backed by storage, grid upgrades, and market reform—offers a more competitive and sustainable path forward.

The recent power outage has intensified opposition to the gradual closure of nuclear power plants. But those who blame renewables and advocate for nuclear as the solution lack evidence to support their claims. The causes of the blackout are likely multiple and complex, and diagnosing them will require rigorous technical analysis.

Nuclear supporters argue that Spain cannot do without a technology with “very competitive real operating costs” (according to Foro Nuclear), and that closing plants by 2035 would raise electricity prices by €13/MWh, increase gas generation, and emissions (according to PWC). But is this undeniable?

Consumers have paid for nuclear energy at market prices, which mostly reflected gas generation costs rather than nuclear’s. So the real beneficiaries of these “very competitive” costs were the owning companies, through increased profits. From the closure agreement in 2019 to 2024, nuclear plants received an average market price of €85/MWh—well above their costs, even including taxes.

The final nuclear closures (Vandellós II and Trillo) aren’t expected until 2035. Ten years is an eternity in energy and tech terms. Estimating electricity market prices that far ahead is extremely complex. How many data centers will connect to the grid? How much electricity will AI consume? How much hydrogen will be produced with renewable power? Will transport and industry be electrified? Will the energy efficiency goals in the PNIEC be realistic? What will gas and CO₂ prices be, both highly volatile? How much investment will go into renewables, storage, and interconnections? Some scenarios suggest the nuclear shutdown could significantly impact prices, while others foresee minimal effect.

Forecasts should not assume a static reality. Closing nuclear plants would open up room for new investments in renewables and storage that wouldn’t be profitable if nuclear plants kept operating. Also, nuclear’s inflexibility hampers the integration of renewables, leading to energy curtailments—cheap, clean power going to waste. Therefore, a gradual nuclear phaseout doesn’t necessarily mean a proportional increase in gas use or emissions.

Beyond the uncertainty of the future, there’s a key counterargument to the idea that electricity would get much more expensive without nuclear: if that were true, power companies would be the most interested in shutting them down. Their gas plants would operate more, and at higher prices, boosting profits across their portfolios.

In reality, companies understand that in a market dominated by renewables, it isn’t profitable to extend the life of nuclear plants. The reason is low market prices—not taxes, which only partially internalize nuclear’s external costs (like waste management and decommissioning). Removing those taxes would amount to subsidizing nuclear power.

So, behind the anti-closure campaign, there may not just be a desire to extend nuclear plant lifespans, but to do so with tax cuts or a guaranteed above-market compensation. Electricity market design has not been challenged by these companies while they were being paid gas-driven prices for all their production. But now that renewables are setting much lower prices, the model is being questioned. Moreover, extending nuclear operations would require costly investments due to aging infrastructure, which could ultimately fall on consumers.

We should discuss the future of nuclear energy and the market design transparently and in the public interest. Is extending the life of nuclear plants necessary to ensure power supply? What would the cost be to consumers? And do nuclear’s supposed benefits outweigh the increasingly complex waste management costs and the (however small) risk of a nuclear accident?

For economic policy, the key question is: how do we enhance competitiveness through lower energy costs? By extending nuclear lifespans, or by betting on mass deployment of renewables, energy storage, and interconnections, with gas as backup?

The energy transition is a key competitive lever. Renewables—alongside storage and interconnection—lower electricity costs for both households and industry. A smart rollout of these technologies and the electrification they enable can also create jobs and strengthen the industry.

Mario Draghi has noted that high energy prices are a major drag on Europe’s competitiveness. In Spain, we have the natural resources to turn that historic curse into a blessing: sun, wind, water, and land to develop renewables. Will we keep importing gas and uranium, or harness our domestic renewables as a lever for industrialization, job creation, investment, and growth?

Energy supply security is non-negotiable. But there’s no evidence that renewable-dominated markets are more vulnerable to supply disruptions. Nor is there technical justification for extending nuclear operations as a backup to renewables. On the contrary: nuclear’s inflexibility prevents adapting to renewables’ variability, making the system less secure and efficient than with more flexible alternatives. And in a total blackout, nuclear is not useful for quick grid restoration.

If we want a reliable, economically and environmentally efficient electricity system, we need to reinforce it. Invest more in renewables, a stronger grid, storage, and interconnections. Do it under the coordination of a Transmission System Operator with full capabilities. And redesign the electricity market to reflect the real cost and value of each technology, reducing uncertainty for investors. Let’s not sacrifice our best opportunity for competitiveness for the sake of interested diagnoses.

Natalia Fabra Professor of Economics, Universidad Carlos III de Madrid Director, EnergyEconLab (funded by the European Research Council)

El pasado 8 de julio tuvo lugar la presentación del Reporte de Economía y Desarrollo (RED) “Energías Renovadas: Transición Energética Justa para el Desarrollo Sostenible” del Banco de Desarrollo de América Latina y el Caribe (CAF).

Esta nueva edición del RED subrayó la necesidad de llevar a cabo una transición energética justa, enfocada desde la perspectiva de América Latina y el Caribe, reconociendo las realidades particulares de cada país en la región y la necesidad de abordar los rezagos históricos del desarrollo.

Este espacio servió como plataforma para la presentación oficial de la nueva edición del RED, y reunió un grupo de expertos de alto nivel para dialogar en torno a propuestas concretas que viabilicen una transición energética justa y sostenible en América Latina y el Caribe.

Consulte la agenda del evento (aquí) y el Resumen Ejecutivo del Reporte (aquí)

Interview with Natalia Fabra (Carlos III University and guest speaker of the XII International Academic Symposium: Accelerating the Net-Zero Economy Transformation) on February 6th, 2023.

El 27 de noviembre de 2023, Natalia Fabra respondió a unas preguntas para #twecos. En este enlace puedes leer la entrevista.

¿La transición energética en España es también una apuesta por el crecimiento económico del país?

La transición energética es un imperativo medioambiental. El futuro de nuestras sociedades no es compatible con el ritmo actual de emisiones contaminantes a la atmósfera, y es también un imperativo económico, porque sin ecología no hay economía… No olvidemos el daño que generan los riesgos climáticos, como inundaciones, incendios, elevación de nivel del mar, olas de calor…, sobre nuestras economías, y los costes de la adaptación al cambio climático. Tampoco olvidemos que, mientras que invertimos en mitigación para cambiar nuestro sistema energético, como inversiones en renovables, redes energéticas, almacenamiento, infraestructuras para la producción y la recarga de los vehículos eléctricos, para la producción del hidrógeno verde, etcétera, estamos también impulsando la economía a través de la generación empleo y de tejido industrial y empresarial. No estamos por tanto ante una disyuntiva entre economía y medio ambiente, sino ante una relación de complementariedad.

¿Cómo podría afectar al suministro energético la prolongación de la guerra en Ucrania?

El suministro energético en Europa no está en juego. Lo hemos visto durante las peores fases de la crisis. Europa ha sido capaz de sustituir la mayor parte de las importaciones de gas ruso con importaciones de gas natural licuado procedente de diversos países. A ello también ha contribuido la reducción del consumo energético y el aumento de la producción de energías renovables, que han permitido desplazar parte de la generación eléctrica con gas. No obstante, esto no quiere decir que los mercados energéticos en Europa sean inmunes a la guerra en Ucrania y a una no deseable prolongación del conflicto. Aún cuando el suministro energético no esté en peligro, las tensiones se traducen en aumentos de precios del gas, que se acaban traspasando a los mercados eléctricos porque, bajo su diseño todavía vigente, en un buen número de horas se paga toda la electricidad a precio de gas. Antes del conflicto, el gas rondaba los 18-20 €/MWh y la electricidad los 40-45€/MWh. Todavía hoy los precios del gas y la electricidad duplican esos valores. En 2022, el gas llegó a superar los 200€/MWh y el precio de la electricidad también se hubiera multiplicado por diez si el gobierno no hubiera puesto en marcha la solución ibérica. Si no queremos que se vuelvan a repetir estos periodos de elevados precios energéticos, que alimentan la inflación y la pobreza energética, y merman la competitividad de las empresas, tenemos que apostar con mayor ambición por las energías renovables, cuyos costes no están sometidos a las fluctuaciones de los precios de los combustibles fósiles, y por nuevos mecanismos regulatorios y de mercado que permitan a los consumidores beneficiarse de los menores costes de las renovables. Hasta que esto no ocurra, nuestras economías seguirán siendo vulnerables, a través de sus efectos sobre los mercados energéticos, a shocks de diversa índole. Ahora son conflictos bélicos, pero en el futuro pueden ser otros cisnes negros.

¿Qué elementos son imprescindibles en la defensa de la competencia?

Es imprescindible contar con una autoridad de competencia independiente, cuyos consejeros sean expertos en economía y derecho de la competencia, y que no tengan que dedicar su tiempo y recursos limitados a tomar decisiones que pertenecen a otros ámbitos, como energía, telecomunicaciones, transporte… La especialización aporta criterio, y el criterio, independencia. También es imprescindible que la autoridad de competencia disponga de recursos suficientes para contratar a personal cualificado, capaz de estudiar las decisiones con el rigor que aporta la economía y el análisis estadístico, con el fin de analizar de oficio sectores susceptibles de presentar problemas de competencia y poner en marcha campañas de promoción de la competencia, con capacidad para sancionar debidamente las infracciones sin que sus sanciones se pongan repetidamente en cuestión. Para ello, también es necesario disponer de tribunales especializados.

¿Qué importancia tiene la investigación en el mundo económico?

Parece un lugar común decir que la investigación debe jugar un papel fundamental, aunque a veces se olvide a la hora de priorizar los recursos que se dedican a ella. En el campo de la economía, la investigación nos permite comprender y cuantificar. Comprender por qué se producen ciertos fenómenos de diversa índole, como el encarecimiento de los precios, la persistencia de la pobreza, el deterioro del medio ambiente… Comprender qué políticas públicas deben ponerse en marcha para paliar los efectos negativos y potenciar los positivos, como diseñar la política de defensa de la competencia para evitar aumentos injustificados en los márgenes empresariales, diseñar un sistema fiscal más equitativo que reduzca las desigualdades, fomentar las inversiones en energías renovables y movilidad sostenible… Y guiar ese proceso de aprendizaje e identificación de los mecanismos que operan en cada caso con la cuantificación, para que la evidencia empírica ayude, lo cual no quiere decir que monopolice, a la toma de decisiones. Para que la investigación sea útil, es imprescindible que se haga desde la independencia. Y para ello, la financiación pública es indispensable. Esto también conviene no olvidarlo.

¿En qué áreas de investigación se ha especializado usted y con qué retos se ha enfrentado a la hora de desarrollar su trabajo?

Mi investigación pertenece al campo de la Economía Industrial, un campo muy amplio que estudia el funcionamiento de los mercados y el diseño de las políticas regulatorias, teniendo en cuenta que los agentes económicos –las empresas, los hogares- en muchas ocasiones se comportan de forma estratégica, esto es, teniendo en cuenta el efecto de las decisiones propias sobre las de los demás. A este campo pertenecen mis dos áreas de especialización, la Economía de la Regulación y la Competencia, y la Economía de la Energía y el Medio Ambiente, que a menudo combino para comprender, por ejemplo, cómo diseñar la regulación de los mercados eléctricos para potenciar la competencia, entre otros objetivos. Haber trabajado en este campo durante los últimos 25 años ha sido apasionante, porque me ha permitido presenciar y analizar los profundos cambios que han vivido los mercados energéticos y su regulación en este tiempo. La transición energética introduce nuevos retos para la regulación de estos sectores y para el diseño de las políticas públicas que permitan acelerar el cambio en la matriz energética de forma justa. Me siento afortunada por haber podido contribuir con mi investigación al debate y a la toma de decisiones en este ámbito tan relevante.

El pasado 17 de noviembre, José Antonio Montenegro entrevistó a Natalia Fabra sobre la importancia de la energía renovable y cómo sustituir los combustibles fósiles en Europea, y la profesora expuso tres ideas de cómo asegurar un futuro con un medio ambiente más limpio.

Pincha aquí y aquí para ver distintas partes de la entrevista.

David Andrés-Cerezo wrote this post on uc3nomics Blog, based on research by David Andrés-Cerezo and Natalia Fabra.

Renewable energy sources, such as solar and wind, are becoming increasingly popular to reduce our dependence on fossil fuels. However, these sources are also highly volatile, as their output fluctuates significantly across time and weather conditions: a solar farm cannot generate electricity after the sun sets, and a windmill does not run on calm days. Grid reliability requires that supply always meets demand, but the volatility of renewable energies makes it challenging. For this reason, energy systems worldwide seek solutions to shift supply from periods with abundant renewable energy to those when it is relatively scarce. This is where energy storage technologies come in. These technologies, including batteries, pumped hydro, and compressed air, are a remedy to counteract the variability of renewable energy sources. Moreover, their investment costs have sharply declined, making storage a potentially attractive option for promoting a quick and cost-effective energy transition.

Policy options and regulatory debate

How can renewable energies and storage technologies be encouraged? Is it enough to rely on market incentives, or are other support measures needed? The dramatic decline in the cost of renewable energy investments has promoted a rapid deployment of these technologies. In turn, the volatility of renewable energies will likely enlarge price arbitrage opportunities for firms looking to invest in storage. Finally, the availability of grid-scale storage will boost the value of renewable assets by reducing curtailment in periods when renewable production is large relative to demand. So, is that it?

This logic suggests that renewable energy and storage are complementary technologies, which reduces the need for further support. Still, regulators worldwide are implementing various policies to encourage investments in renewables and storage. For instance, the California Public Utility Commission has implemented a mandate requiring utilities to procure energy storage. Similarly, several European countries, such as Spain, are mandating battery investment as an eligibility requirement for renewable energy subsidies. Beyond the standard goal of correcting environmental externalities, these policy interventions may be motivated by coordination failures that prevent a quick transition to carbon-free power markets. But, are these policies equally effective at every stage of the energy transition? Should they be tailored to the characteristics of each market, such as their solar potential? How do policies to support one technology affect investment incentives for the other?

Modeling electricity markets with energy storage

In a recent article with Natalia Fabra, we seek to answer these questions by modeling investment and operation decisions in wholesale electricity markets. We then quantify the theoretical predictions with simulations of the Spanish electricity market under two scenarios with low and high renewables penetration and different levels of storage capacity.

In our theoretical model, competitive storage and generation firms first decide whether to enter the market and then choose how much to produce and store/release in each hour of each day. Storage operators benefit from arbitraging price differences over time: they buy (charge their batteries) when prices are low and sell (discharge their batteries) when prices are high. The availability of renewable energy affects their profitability as renewables generation might depress prices when the storage facilities charge (in this case, the profitability of storage goes up) or when they discharge (its profitability goes down). Likewise, storage affects the profitability of renewables positively or negatively depending on whether storage operators charge their batteries (which increases prices) or discharge them (which reduces prices) when more renewables are available.

How do we know whether renewables make energy storage operators better or worse off, and vice-versa? Our model predicts that the correlation between renewable availability and market prices is key to explaining their relationship. A negative (positive) correlation means that renewables tend to be available when prices are low (high), which is when storage charges (discharges), thus pushing up (down) the prices at which renewables sell their output, increasing (decreasing) their profitability. Similarly, if this correlation is negative (positive), deploying renewable capacity depresses prices when storage charges (discharges), thus increasing (decreasing) the profitability of storage.

When should we then expect this key correlation to be positive or negative? Electricity prices depend on consumption patterns and solar and wind availability patterns, which vary across markets. Hence, the sign of the correlation between prices and renewables is an empirical question. For this reason, we explore the interaction between renewables and storage in a given context: the Spanish electricity market.

Simulating the Spanish wholesale electricity market

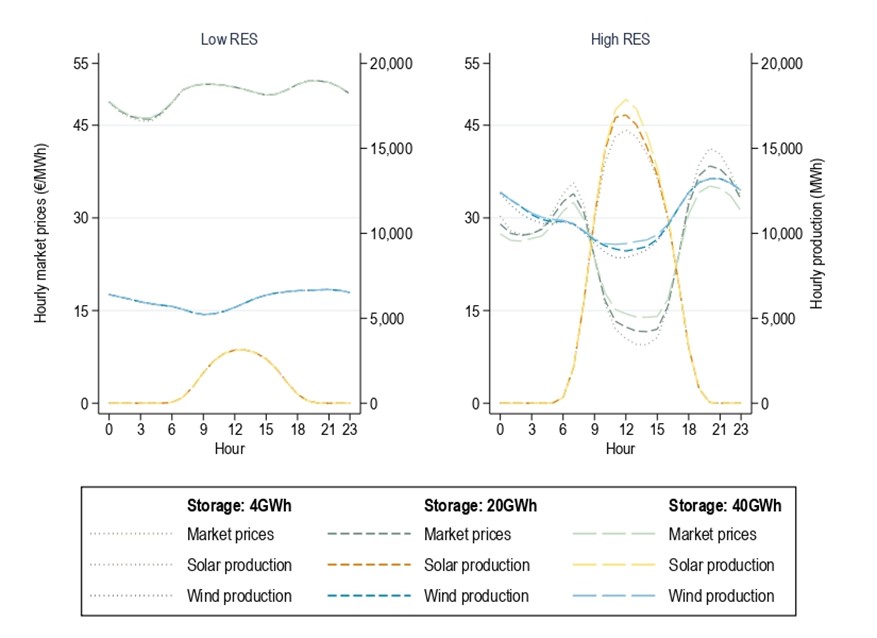

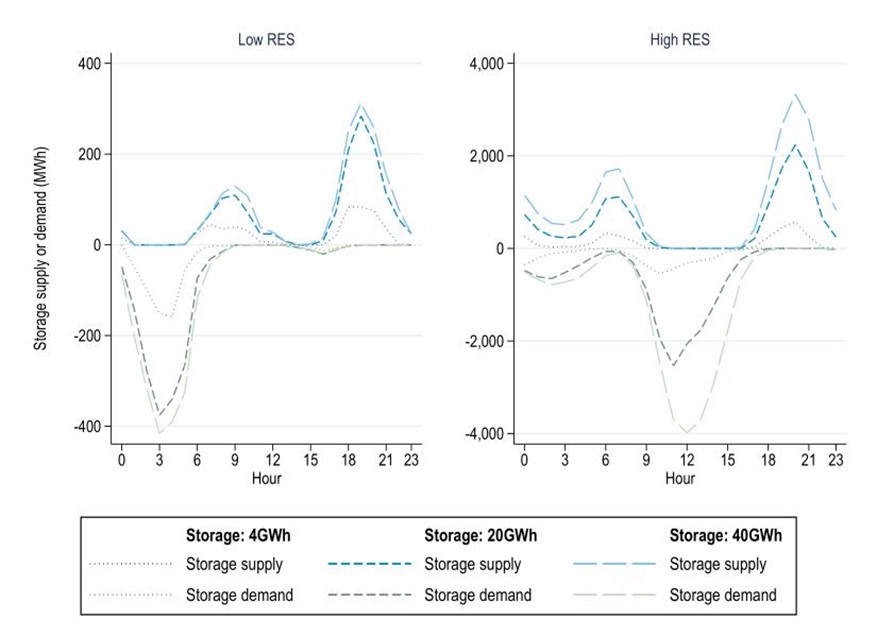

We consider two scenarios: the Spanish electricity market as of 2019, when renewable penetration was relatively low (8.7 GW of solar and 25.6 GW of wind), and the market as it is expected by 2030, when solar and wind capacities are planned to reach 38.4 GW and 48.5 GW, respectively. For each scenario, we consider various levels of storage capacity from 4 GWh to 40 GWh. Figure 1 shows wind and solar production and electricity prices over an average day in 2019 (left panel) and 2030 (right panel). Figure 2 displays (average) hourly storage and release decisions in these two scenarios.

Figure 1: Prices and renewable generation over the day

Figure 2: Charging and discharging decisions over the day

Let us focus on solar production. Figure 1 shows that solar production is concentrated in the intermediate hours of the day. This implies that solar is positively correlated with prices when there are few solar farms (left panel), as solar peaks at noon when consumers’ demand is high. When solar production becomes abundant (right panel), the correlation between prices and solar production becomes strongly negative, as solar generation depresses market prices when available. As a result of this price impact, storage firms shift from charging during nighttime when solar penetration is low (left panel) to charging in the midday hours when solar generation is abundant (right panel).

What does this behavior imply for the profitability of solar plants and storage firms in the Spanish electricity market? At the early stages of the renewable deployment (left panel), entry by an additional solar farm has a negligible impact on storage profits, as the price at which storage charges during the night remains unchanged and solar production does not affect the prices at which storage firms sell their output. Similarly, adding storage capacity has no price impacts at times of solar availability. Hence, the profitability of solar and storage investments remains independent despite the positive correlation between prices and renewables.

However, a big expansion in solar capacity has two effects: it enlarges price differences across the day and makes the correlation between prices and solar production turn negative. As a result, battery utilization increases, and storage profits climb sharply. Similarly, increasing storage capacity from 4 GWh to 40 GWh substantially increases prices in midday hours when storage firms are filling their batteries. Since this coincides with the periods in which solar farms produce energy, their profits go up. This is further compounded by storage allowing more efficient use of solar assets since it reduces energy spills in periods of abundant solar production.

Policy implications

In sum, whether renewables and storage complement or substitute each other might vary from one market to another and differ across time. Policies to promote these technologies should evolve accordingly. In the early stages of solar capacity adoption, prices are typically positively correlated with solar production. Since solar generation is not abundant, it has no price impacts, and the profitability of storage remains independent of how much solar capacity there is. At later stages of the Energy Transition, solar generation depresses prices, turning the correlation between solar generation and prices negative. This implies that increasing storage makes solar firms better off, and increasing solar capacity makes storage firms better off, i.e., they become complements once the correlation is reversed.

Therefore, our findings suggest that a big initial push for renewable investment is necessary to trigger the complementarity between renewable energy and storage. Once the negative correlation kicks in, policies aimed at promoting one technology would come with the additional benefit of promoting the other, shifting the market to a more decarbonized long-run equilibrium.

But this does not set the question once and for all! Future electricity markets may have very different demand and supply patterns from those of today. Therefore, policy design should pay close attention to the specific characteristics of each market at different stages of the energy transition and evolve with it.

Further Reading:

Andrés-Cerezo, and D. Fabra, N. (2023) “Storage and Renewable Energy: Complements or Substitutes?”, Working paper.

About the authors:

David Andrés-Cerezo is Visiting Professor Carlos III University and EnergyEcoLab. He is interested in Energy and Environmental Economics, and Political Economy.

Natalia Fabra is an industrial economist working in the field of Energy and Environmental Economics. She is Professor of Economics at Carlos III University.

Last April 17, Mateus Souza wrote this post on uc3nomics Blog, based on research with Peter Christensen, Paul Francisco, Erica Myers, and Hansen Shao.

Improving the energy efficiency of buildings is often viewed as one of the most promising strategies for climate policy. Retrofit and renovation programs have great potential to abate carbon emissions by lowering households’ energy consumption, which also translates into lower energy bills. These programs can also improve air quality within homes (Tonn, Rose, and Hawkins, 2018) and may even help create jobs (ORNL, 2014). Given all these potential benefits, renovation projects are taking a central role in economic stimulus packets for decarbonization, and for recovering from the recent energy and COVID-19 crises. For example, through the EU’s Recovery and Resilience Facility (EC, 2022), Spain intends to “(support) the green transition through investments of over €7.8 billion in the energy efficiency of public and private buildings.” Similarly, the U.S. Inflation Reduction Act (White House, 2023) projects investments of “$9 billion for states and Tribes for consumer home energy rebate programs, enabling communities to make homes more energy efficient, upgrade to electric appliances, and cut energy costs.”

However, economic evaluations have found that the energy savings from these programs often do not meet expectations. In some cases, the average savings may be as low as 30% of the expected savings (Fowlie, Greenstone, and Wolfram, 2018). This substantially lowers the cost-effectiveness of these programs and puts into question their role in climate policy. Mateus Souza and co-authors dig into this issue with two recent articles. The first helps to identify economic and behavioral explanations of why a “performance wedge” exists between the projected versus the realized energy savings of efficiency programs (Christensen et al., 2021). The second asks whether it is possible to use machine learning tools to improve projections of energy savings, with the objective of better targeting funds to homes that are more likely to benefit from the programs (Christensen et al., 2022).

Decomposing the wedge

To better understand the “performance wedge” in energy savings, we studied the Illinois Home Weatherization Assistance Program (IHWAP). The program provides fully subsidized improvements to the heating, ventilation, and air conditioning (HVAC) systems of low-income family homes in the state of Illinois. We analyzed detailed program information, including data on housing structure, demographics, and energy consumption for more than 9,800 homes. Using a novel machine learning-based approach (Souza, 2019), we investigate the importance of three channels that may explain the wedge: 1) systematic bias in engineering measurement and modeling of savings, 2) work quality during installation of the upgrades (workmanship), and 3) the rebound effect (savings may be offset in case households systematically increase their thermostats once the system becomes more energy efficient).

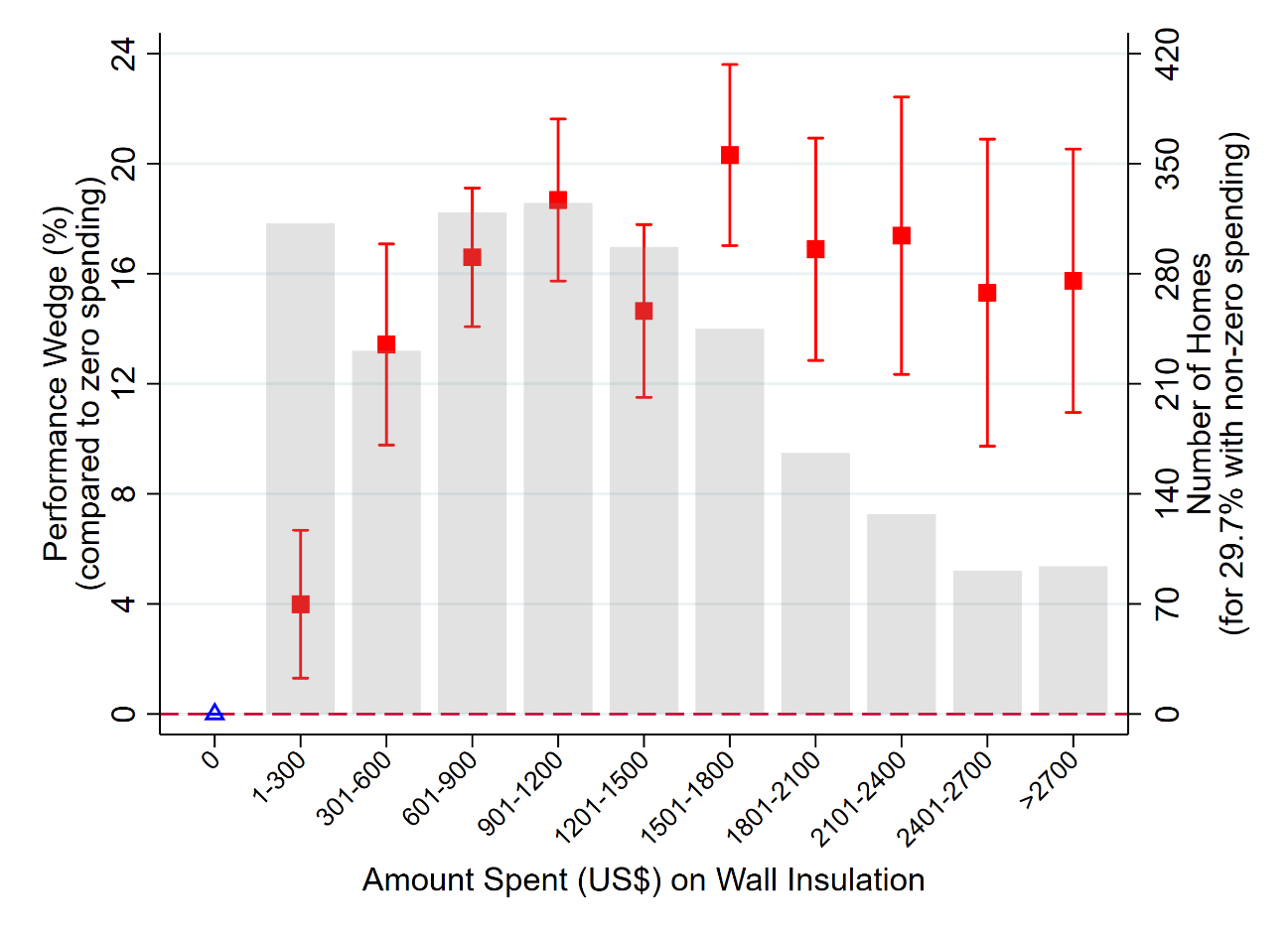

Results suggest that bias in model projections is one of the primary contributors to the wedge. Up to 41% of the wedge can be explained by discrepancies between projected and realized savings in five major retrofit categories: air sealing, furnace replacement, wall insulation, attic insulation, and windows. Results are particularly striking for wall insulation, as shown in Figure 1. The red squares are point estimates of how the performance wedge increases depending on expenditures in that measure, compared to homes that received zero wall insulation spending. The whiskers represent 95% confidence intervals. The figure shows, for example, that the wedge is approximately 20 percentage points higher for homes with wall insulation expenditures between $1,501 and $1,800.

Figure 1: Increased Performance Wedge by Spending on Wall Insulation

Heterogeneity in workmanship is also an important factor in explaining the wedge. Results suggest that the wedge could be reduced by up to 43% if all workers performed at top levels. This implies that there exist potential gains from changing worker incentives, investing in contractor training, etc. On the other hand, only a modest portion of the wedge may be explained by behavioral factors such as the rebound effect. Using data on the realized relationship between outdoor air temperature and energy consumption, we find that households modestly increased their thermostats after weatherization, accounting for only up to 6% of the wedge.

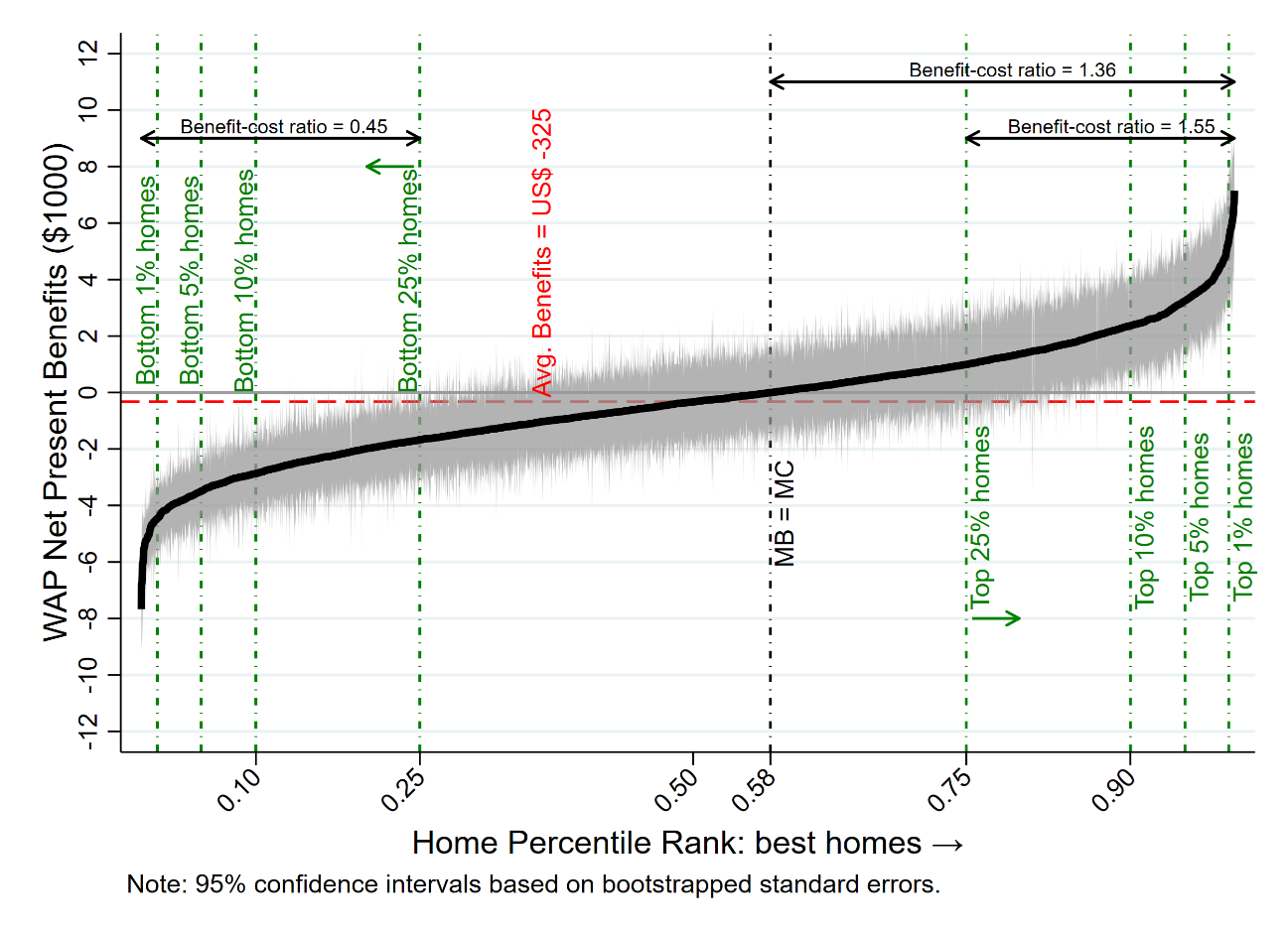

We also analyze the program’s cost-effectiveness by comparing the energy and carbon abatement benefits versus the costs of the retrofits. We find that, on average, each home the program serves is associated with net benefits of -$325. Although average net benefits are close to zero, disaggregated estimates reveal substantial heterogeneity, such that approximately 42% of homes generate positive net benefits, as shown in Figure 2. Therefore, certain types of projects are highly cost-effective, suggesting a potential role for targeting in this context.

Figure 2: Net Present Benefits of Retrofitted Homes

Potential gains from targeting

Within this context of substantial heterogeneity in net benefits, a natural follow-up question is whether it is possible to identify the high-return projects before they are actually implemented. We conducted another analysis with data from the same program but now using information available only before the homes were retrofitted. The idea is to mimic the role of a program implementer who is trying to predict the magnitude of net benefits prior to performing the retrofits. To maximize the total predicted net benefits from the program, the implementer would then choose to treat only homes with positive expected returns. This consists of an ex-ante prediction/targeting exercise, which differs substantially from an ex-post evaluation performed with information available many months after the renovations.

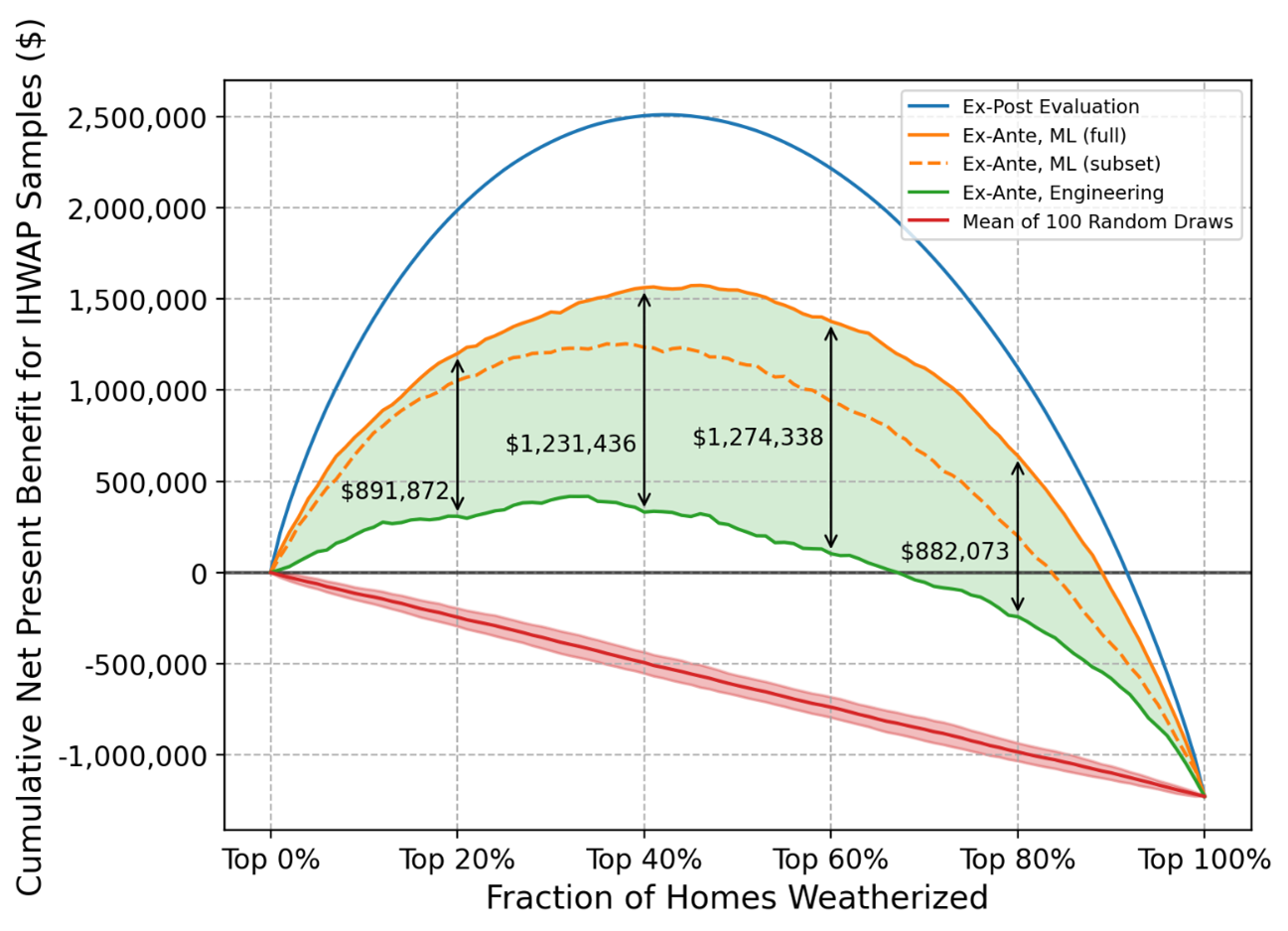

As a first step, we show that it is possible to accurately predict home-specific energy savings from the program by using machine learning techniques. In fact, we find that our predictions are accurate even when using a subset of publicly available variables (such as the size and the age of the home, the number of rooms, and the presence of an attic). We then rank homes from highest to lowest net present benefits and calculate the cumulative monetary benefits from retrofitting homes in that order. These results are presented in Figure 3. We compare our machine learning rankings (in orange) to an engineering ranking (in green) that currently guides funding allocation decisions within the program. These are also compared to a ranking with perfect foresight (in blue). Results show that the machine learning strategy outperforms the engineering model and could drastically improve program cost-effectiveness. Within this sample, targeting high-return interventions based on machine learning predictions can dramatically increase net benefits from $0.93 to $1.23 per dollar invested.

Figure 3: Potential Gains from Targeting

Conclusions

Thanks to recent advances in information and data technologies, retrofit programs can readily incorporate machine learning-based strategies to help select among candidate projects. Energy efficiency programs are often sponsored by utilities that have recently developed the data infrastructure to store, query, and serve household billing data. Integrating predictions from machine learning models into those infrastructures would be straightforward. Although these models may be computationally demanding, they only need occasional updates. Once the results are obtained, they can be fed into the backend of existing software that already help with funding allocation decisions.

The importance of considering and implementing these types of tools continues to grow as energy efficiency remains central to climate policy discussions. Optimal allocation of these funds may be crucial to achieve ambitious climate goals. Future work within this context has yet to explore, for example, the distributional implications of targeting investments based solely on energy or climate-related benefits. Analyses of the health and potential job creation impacts of these programs also seem mostly missing from the economic literature.

Further Reading:

Peter Christensen, Paul Francisco, Erica Myers, and Mateus Souza (2021). “Decomposing the Wedge between Projected and Realized Returns in Energy Efficiency Programs.” The Review of Economics and Statistics (Forthcoming); https://doi.org/10.1162/rest_a_01087

Peter Christensen, Paul Francisco, Erica Myers, Hansen Shao, and Mateus Souza (2022). “Energy Efficiency Can Deliver for Climate Policy: Evidence from Machine Learning-Based Targeting.” NBER Working Paper 30467; https://www.nber.org/papers/w30467

Mateus Souza (2019). “Predictive Counterfactuals for Treatment Effect Heterogeneity in Event Studies with Staggered Adoption.” SSRN Working Paper 3484635; EEL Discussion Paper 107; https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3484635

About the authors:

Mateus Souza is a Postdoctoral Researcher at EnergyEcoLab, Department of Economics, Universidad Carlos III de Madrid.

Hansen Shao completed his PhD in Economics in 2021 at the University of Illinois at Urbana-Champaign, and is currently an economic consultant based in China.

Fowlie, Meredith, Michael Greenstone, and Catherine Wolfram (2018). “Do Energy Efficiency Investments Deliver? Evidence from the Weatherization Assistance Program”. The Quarterly Journal of Economics 133, 1597-1644; https://academic.oup.com/qje/article/133/3/1597/4828342

Oak Ridge National Laboratory (2014). “Weatherization Works – Summary of Findings from the Retrospective Evaluation of the U.S. Department of Energy’s Weatherization Assistance Program”. ORNL Technical Report 2014/338; https://nascsp.org/wp-content/uploads/2017/09/ORNL_TM-2014_338.pdf